Private equity secondaries: What they are and the opportunity for investors

In this blog, we cover the basics of private equity secondaries and why 2026 may be a potentially attractive time to invest in secondaries.

Most investors are familiar with private equity as a strategy for accessing companies before they go public. But there's a distinct and rapidly growing segment of the market — private equity secondaries — that operates differently and is attracting significant attention from institutional and accredited investors alike.

In this blog, we breakdown:

- What are private equity secondaries?

- How have private equity secondaries historically performed?

- Why 2026 may be a potentially attractive time to invest in secondaries

- What are the risks of investing in secondaries?

- How Heron Finance’s private equity strategy is positioned for secondaries

Get a diversified private markets portfolio built to weather market volatility.

What are private equity secondaries?

Private equity secondaries involve the purchase and sale of existing ownership interests in private equity funds or companies. Unlike primaries private equity investing — where investors commit capital to a new fund or company at inception — secondaries buyers acquire stakes from current holders, often at a discount, gaining exposure to a portfolio of identifiable, funded assets that are already in operation.

There are two main types of secondaries transactions:

- LP-led secondaries: An existing limited partner (LP) sells their fund stake to a new investor seeking to acquire the exposure.

- GP-led secondaries: A general partner (GP) transfers one or more high-conviction assets into a new continuation vehicle, giving existing investors the option to exit or roll over, and offering new investors entry into assets that already have a verifiable performance history and fund-management continuity.

A brief history of private equity secondaries

While private equity secondaries have gained significant momentum in recent years, the strategy traces back to the 1990s, with pioneers like Coller Capital, Landmark Partners (now part of Ares), and Lexington Partners (now part of Franklin Templeton) institutionalizing the market. Today, the secondaries market has evolved into a critical source of liquidity across private markets, especially with respect to private equity transactions.

Private equity investing: Comparing primaries vs. secondaries

Note: Characteristics shown are general market observations and are not intended to suggest that all private equity primary or secondary investments will exhibit these features. Actual investment terms, timing of cash flows, diversification, pricing relative to NAV, and return profiles vary by fund, market environment, manager, and transaction structure.

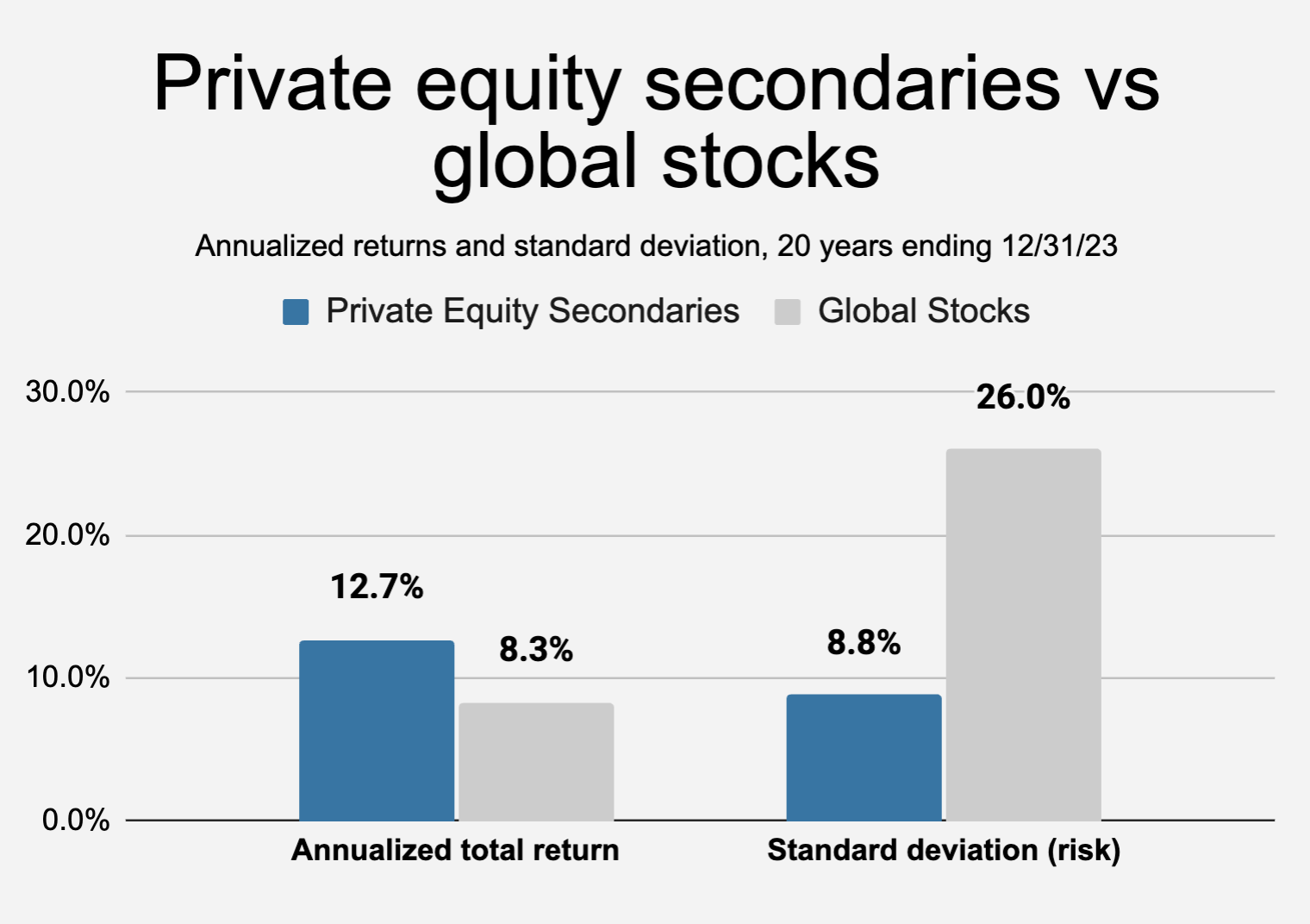

How have private equity secondaries historically performed?

Secondaries have historically delivered higher returns with lower risk (as measured by standard deviation) compared to global stocks:

In addition to historically outperforming global stocks as we see in the chart above, according to Coller Capital, citing Preqin data, secondaries generated the highest median net internal rate of return (IRR) of any private market type, and at a lower standard deviation than other private equity strategies, based on private market investments with vintage years (when a fund was initiated) from 2004 to 2023

How secondaries reduce the "J-curve" drag

Private equity secondaries also tend to reduce the "J-curve" drag typical in primaries private equity investing.

Here's what this means in general terms:

- Private equity primaries may experience flat or negative returns during the early years of a fund. This is often due to management fees, fund expenses, and transaction costs being incurred before the underlying portfolio investments have had sufficient time to mature and generate realized gains.

- Private equity secondaries may reduce or shorten this early-period effect because they typically involve acquiring interests later in a fund’s lifecycle, often after capital has already been deployed into more seasoned portfolio assets. As a result, secondaries may provide a shorter path to distributions and may lessen the duration of the flat or negative return profile often associated with primary investments.

Why 2026 may be a potentially attractive time to invest in secondaries

A combination of structural and market-specific factors is making this an environment many investors are watching closely for secondaries opportunities.

- Companies are staying private longer. The median age for company IPOs reached 14 years in 2024, up from just six years in 2000.

- Supply is outpacing capital. The supply of private equity sellers is, for now, outpacing the supply of buyers. Neuberger Berman notes that private equity exit activity remains more than 50% below 2021 peaks and distributions to investors have fallen to historic lows — creating growing pressure among existing private equity holders to find liquidity. Secondaries transaction volume reached $240 billion in 2025 across the private markets, up 48% year-over-year, yet available secondaries capital stands at approximately $215 billion — roughly one year of transaction volume, compared to the three to four years of coverage typical in primaries private equity markets.

- An increasingly viable exit option: Secondaries represented approximately 20% of total global private equity exit activity in 2024, up from just 7% in 2020, based on data from Pitchbook and Jefferies, highlighting the growing importance of the market as a liquidity source.

- Market uncertainty may create wider discounts. Franklin Templeton observes that current geopolitical tensions — including the recent U.S.-Israel conflict with Iran — are expected to further slow private equity exits and M&A activity, deepening the structural need for liquidity among existing investors. In this environment, secondaries managers may be positioned to acquire stakes in performing assets at potentially attractive discounts to net asset value (NAV).

- The market is still early relative to its potential. Coller Capital projects that the secondaries market — which has grown at a 16% compound annual rate over the past decade — could reach $500 billion in annual transaction volume by 2030, roughly double today's levels.

What are the risks of investing in secondaries?

Like all private market investments, secondaries investing carries risks:

- Illiquidity: Capital may be locked up with limited options to exit.

- Valuation complexity: Private assets are generally priced using GP-reported NAVs and appraisals rather than real-time market data, which introduces uncertainty. Assets acquired at discounts to NAV can still underperform if the fundamentals of underlying companies deteriorate.

- Manager selection risk: Return dispersion across secondaries managers is significant. Deal sourcing relationships, underwriting discipline, and experience across market cycles are critical differentiators.

- Due diligence complexity: While secondaries investing benefits from visible asset holdings and history, due diligence is primarily focused on the quality and track record of the fund managers, not on deep re-underwriting of underlying individual assets.

By understanding these risks, investors can make sound choices for their portfolio allocation.

How Heron Finance’s private equity strategy is positioned for secondaries

Heron's private equity strategy provides allocations to both the primaries and secondaries markets. With a global portfolio of seven funds, ~500 GPs via secondaries exposures, and 7,000+ underlying portfolio companies, we believe our private equity program is well positioned to capitalize on the structural and cyclical factors that are driving opportunities in secondaries right now.

As with all of our strategies, we apply a proprietary fund manager selection process focused specifically on identifying managers with demonstrated experience in private equity secondaries — evaluating their deal sourcing relationships, underwriting track record, and ability to navigate different market environments.

Get a diversified private markets portfolio built to weather market volatility.

*See original source: https://advisors.voya.com/system/files/system/files/article/file/how-secondaries-are-reshaping-private-equity-market.pdf. The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. The MSCI World Index consists of the following 23 developed market country indexes: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom, and the United States. (https://www.msci.com/world) while Pomona’ focuses on primarily purchasing secondary interests in private equity funds. The MSCI World Index has not been selected to represent an appropriate benchmark to compare an investor’s performance, but rather is shown as a comparison to that of a well-known and widely recognized index. The MSCI World Index is not subject to any of the fees and expenses to which any Pomona fund would be subject and no fund sponsored by Pomona Capital will attempt to replicate the performance of the MSCI World Index. The Cambridge Secondary Funds Index is based on unaudited quarterly performance data compiled from 334 secondary funds (excluding hard assets funds), including fully liquidated partnerships, formed between 1991 and 2023. The index has limitations (some of which are typical to other widely used indices) and cannot be used to predict performance of the Fund. These limitations include: 1. Survivorship bias (the returns of the index may not be representative of all secondary funds in the universe because of the tendency of lower performing funds to not report returns to the index); 2. Lack of transparency (the specific funds that are included in this index are not disclosed by Cambridge Associates, and therefore cannot be independently verified); 3. Heterogeneity (not all secondary funds are alike or comparable to one another, and the index may not accurately reflect the performance of a described style); and 4. Limited data (many funds do not report to indices, and the index may omit funds, the inclusion of which might significantly affect the performance shown). The index does not represent the Fund’s performance, and has not been selected to represent an appropriate benchmark to compare an investor’s performance, but rather is provided to allow for comparison to that of certain well-known and widely recognized indices. Further, as Cambridge Associates recalculates the index each time a new fund is added, the historical performance of this index is not fixed, cannot be replicated, and differs over time from the data presented in this communication. See Cambridge Associates for a complete explanation on IRR calculations and assumptions. The investments within Pomona Investment Fund and the corresponding performance volatility thereof may differ significantly from the securities and or funds that comprise the Cambridge Index, which may contain strategies and asset types Pomona does not utilize. The Cambridge Index is not subject to any of the fees and expenses to which Pomona Investment Fund would be subject and no fund sponsored by Pomona Capital will attempt to replicate the performance of the Cambridge Index. Pomona does not pay any fees to Cambridge Associates to be ranked.

This communication is for informational and educational purposes only and does not constitute investment advice, a solicitation, or an offer to buy or sell any security. Investing in private equity involves significant risks, including illiquidity and the potential loss of principal. This content is intended solely for accredited investors. Past performance is not indicative of future results. Forward-looking statements and market projections cited herein are based on third-party sources and assumptions and are not guarantees of future performance or market conditions. Third-party sources are referenced for informational purposes only and do not constitute an endorsement by Heron Finance.