What Makes Middle Market Loans Attractive for Investors? A Q&A With PGIM

Experts from PGIM explain why core middle market direct lending offers an attractive risk-return profile within the broader credit landscape.

The growing direct lending market may offer investors a compelling opportunity to achieve strong yields and stable returns. However, as the market expands and becomes increasingly segmented, concerns about risk remain a consistent theme among investors evaluating their options.

In this Q&A, we talk with PGIM, part of Prudential's global investment management business and a private credit manager included in the Heron portfolios.

Experts from PGIM help us understand how the dynamics of core middle market direct lending may provide investors with a clearer understanding of why this segment can offer an attractive risk-return proposition within the broader credit landscape.

For starters, what is middle market direct lending?

The middle market, often defined by businesses with annual revenues ranging from $10 million to $1 billion,1 represents a dynamic and relationship-driven segment of the economy.

These businesses are predominantly privately held, often individual- or family-owned, with only a small percentage (approximately 10%2) supported by private equity.

Why might middle market direct lending offer a compelling risk-return profile?

We see three reasons:

- Relationship-Driven Lending Models: Due to ownership structures and company size, the middle market lending environment relies on personal connections and localized expertise. Borrowers value lenders that demonstrate an in-depth understanding of their specific industries, regional nuances and operational complexities. This relationship-centric model provides lenders with direct access to company management, enabling them to gain deeper insight into financial health and operational performance. Such access supports active portfolio management and allows lenders to identify early signs of financial stress, implementing mitigation strategies as needed.

- Conservative Leverage Profiles: Middle market loans have historically exhibited conservative leverage compared to up-market deals. While up-market transactions often feature leverage levels of 5-6x EBITDA, middle market deals typically average 3-4.5x EBITDA.3 This lower leverage profile provides borrowers with greater flexibility in the event of financial distress or downturns, thereby reducing the likelihood of default and enhancing lenders’ ability to protect their investments.

- Covenants and Structural Protections: Another consideration supporting the attractive risk profile of middle market lending is the presence of robust financial covenants and structural protections. Financial covenants provide lenders with regular tests of key metrics to monitor a borrower’s financial health.

Say more about loan covenants, how are those stronger in middle market direct lending?

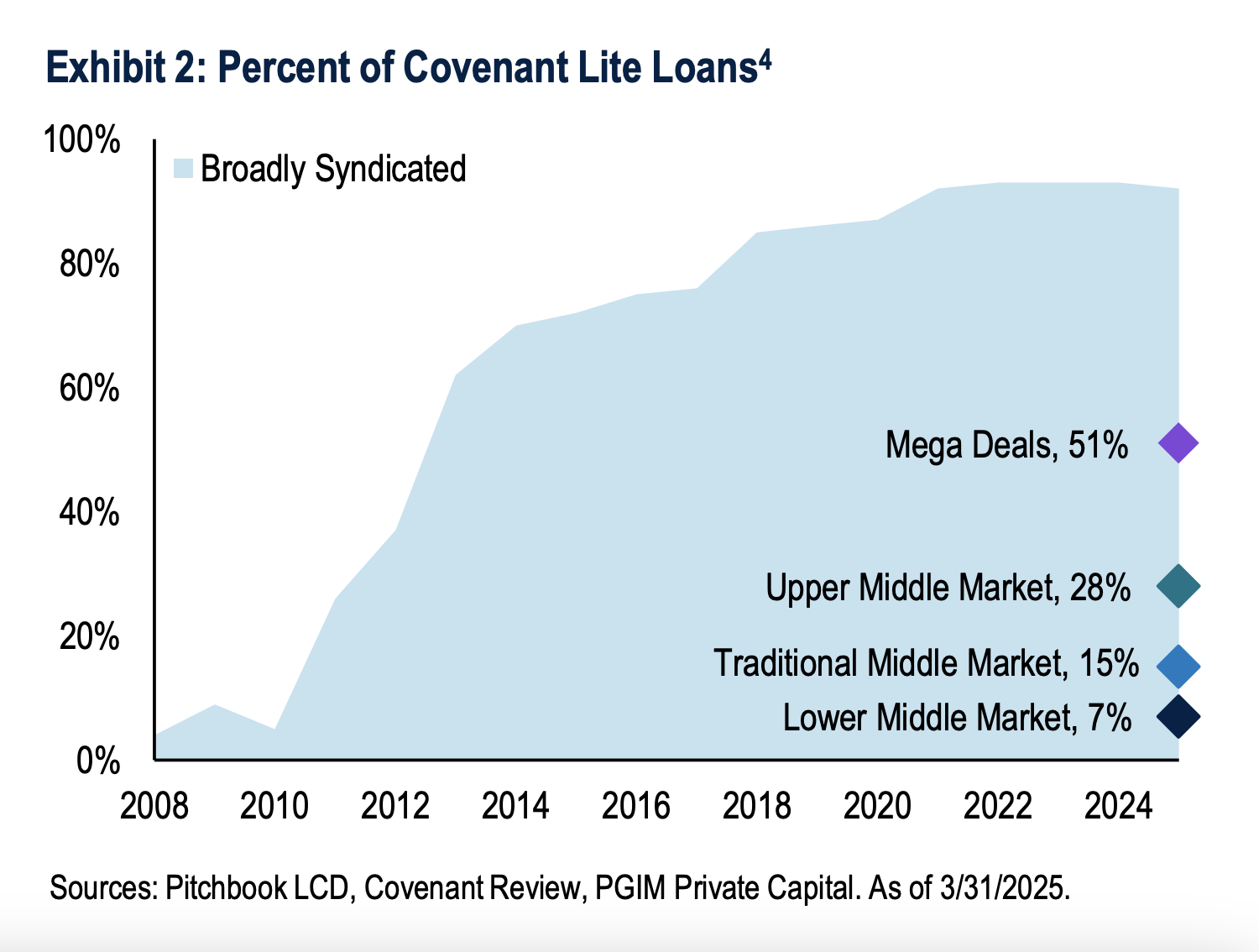

More than 75% of middle market loans include financial covenants, compared to less than 10% of loans in the broadly syndicated loan market, which are typically “covenant lite.” We can see this in the graph below.

Private credit loan Covenants can include:

- Debt / EBITDA: Assesses whether debt is becoming too high relative to earnings.

- Fixed charge coverage: Evaluates whether the borrower’s cash flow is sufficient to cover debt payments, interest and capital expenditures.

- Others such as maximum CapEx or minimum EBITDA: Helps monitor spending discipline and liquidity.

Financial covenants are immensely helpful in acting as early warning systems, allowing lenders to intervene proactively if a borrower’s performance deviates from expectations.

Beyond financial covenants, middle market loans also benefit from stronger documentation. This includes tighter negative covenants that restrict borrowers from actions such as incurring additional debt, paying dividends or making restricted investments – activities that could otherwise erode liquidity and compromise collateral.

What should investors look for when considering an allocation to middle market direct lending?

Ultimately, the success of a direct lending allocation depends on the selection of the right fund manager.

Investors can benefit from partnering with experienced managers who have been through market cycles and understand the nuances of the middle market. Experienced, market-tested managers likely have a disciplined approach to deal structuring and risk management.

For example, a veteran direct lending manager may have years of experience structuring deals and negotiating terms effectively at origination, which is fundamental to helping minimize risk. Underwriting deals with lower leverage and implementing comprehensive covenant packages provide lenders with the tools to identify and mitigate issues before they escalate.

At PGIM, we pride ourselves on experience. We have $1.39 trillion in total assets under management and over 200 clients that we’ve served for more than 20 years. We bring a global perspective with 42 offices on 4 continents. For us, experience is a key differentiating factor as our team has managed assets through 30+ market cycles.

Endnotes:

1. Source: National Center for the Middle Market. As of June 2025.

2. Number of middle market companies sourced from National Center for the Middle Market; number of private equity backed companies sourced from Pitchbook.com; PGIM estimates.

3. Middle market leverage data sourced from Lincoln International. Up-market data sourced from Pitchbook LCD, LBO Quarterly Trend Lines report. As of 12/31/2024.

4. Percent of broadly syndicated covenant lite sourced from Pitchbook LCD, Leveraged Loan Quarterly Trend Lines report. Middle market covenant lite sourced from Covenant Review. As of 3/31/2025.

Disclosure:

The views expressed in this Q&A blog do not necessarily reflect those of PGIM, Heron, their respective affiliates, or representatives. Heron and PGIM do not endorse or guarantee the accuracy or reliability of any statements made. This content is for informational purposes only and should not be considered financial, investment, or legal advice. Readers should conduct their own research and consult a financial advisor before making any investment decisions. Neither Heron nor PGIM is liable for any losses or damages resulting from reliance on this information. All investments involve risk, including the loss of capital.

©The Heron Finance Blog 2025 | The information on this website does not constitute an offer to sell securities or a solicitation of an offer to buy securities. Further, none of the information contained on this website is a recommendation to invest in any securities or a recommendation of any interest in any investment offered by either (i) Warbler Labs, Inc. or any of its subsidiaries (collectively, “Warbler”) or (ii) PGIM, Inc. or any of its affiliates or subsidiaries (collectively, “PGIM”). Any financial forecasts or financial returns, whether in the form of dividends or capital appreciation displayed on this website are for illustrative purposes only and are not a guarantee of future results. Private credit investments are subject to credit, liquidity, and interest rate risk. In the event of any default by a borrower, you will bear a risk of loss of principal and accrued interest on such loan, which could have a material adverse effect on your investment. A borrower may default for a variety of reasons, including non-payment of principal or interest, as well as breaches of contractual covenants. Credit risks associated with the investments include (among others): (i) the possibility that earnings of a borrower may be insufficient to meet its debt service obligations; (ii) a borrower’s assets declining in value; and (iii) the declining creditworthiness, default, and potential for insolvency of a borrower during periods of rising interest rates and economic downturn. No communication by Warbler, PGIM or any of their respective affiliates through this website should be construed or is intended to be investment, tax, financial, accounting, or legal advice. Warbler Advisory, Inc. is an SEC-registered investment advisor (RIA). Such registration should in no way imply that the SEC has endorsed the entities, products or services discussed herein.