Why Private Credit Covenants Matter for Investors: A Q&A With FS Investments

In this Q&A with FS Investments, we explore how private credit loan covenants aim to protect investors.

Private credit can be complex for retail investors and RIAs. One of its many complexities is “covenants” which exist to protect lenders and investors.

To gain a clear understanding of private credit loan covenants, we sat down for a Q&A with FS investments, a private credit manager included in the Heron portfolios.

Generally, what protections are in place for private credit loans to help lenders and end investors?

A loan is governed by a credit agreement, which outlines two very important details:

- Terms of the loan: basic terms of the loan include the maturity, interest rate, spread, and use of proceeds

- Covenants: Rules that govern the actions of borrowers and lenders, ultimately with the goal of protecting lenders and investors.

Loan covenants are essential because they help address a basic conflict in lending: company owners don’t always act in ways that behoove lenders.

These rules give lenders more control over what a borrower can or can’t do – reducing the risk that misaligned interests could hurt the value of the loan or the return on investment.

Loan covenants can be defined in terms of their type – what they purport to regulate – and their structure – how they go about that regulation.

Covenant types include:

- Affirmative: These require borrowers to take certain actions, such as delivering prompt financial statements, maintaining proper insurance, and complying with relevant laws. These are generally standard across credit markets.

- Negative: These limit the ability of borrowers to take certain actions without lender consent. Examples include limits on incurrence of new debt, restrictions on distributions to equity holders, and limits on pledging assets as collateral for other debts.

- Financial: These are tests tied to the borrower’s financial performance. They are designed to ensure the borrower maintains a level of financial health consistent with its ability to meet debt obligations and preserve lender protections. Examples include tests based on leverage ratios and interest coverage ratios.

Covenant structures include:

- Incurrence: These test the financial health of the borrower only in the case of certain borrower actions and are typically utilized in the place of stricter maintenance covenants. For example, they may limit the ability of a borrower to pay distributions or take on new debt unless certain financial thresholds are met.

- Maintenance: These test the financial health of the borrower regularly and require the borrower to maintain financial ratios above a certain level. An example would be a requirement that the borrower maintain a total leverage ratio (debt/EBITDA) below 5x. Failing of a financial maintenance covenant could put the borrower into technical default.

How does the prevalence of these covenants differ across various areas of the leveraged corporate credit market?

The prevalence of covenants varies widely by market, and there are significant differences between public and private credit markets.

- Affirmative covenants are standard inclusions across credit agreements in all markets.

- Negative covenants are universally present, as well, but variations in strictness are key considerations for investors. Negative covenants tend to be tighter in the private credit market compared to public credit, making it more challenging for creative lawyers to find loopholes to take actions such as issuing “super-senior” debt or carving assets out of the existing collateral pool.

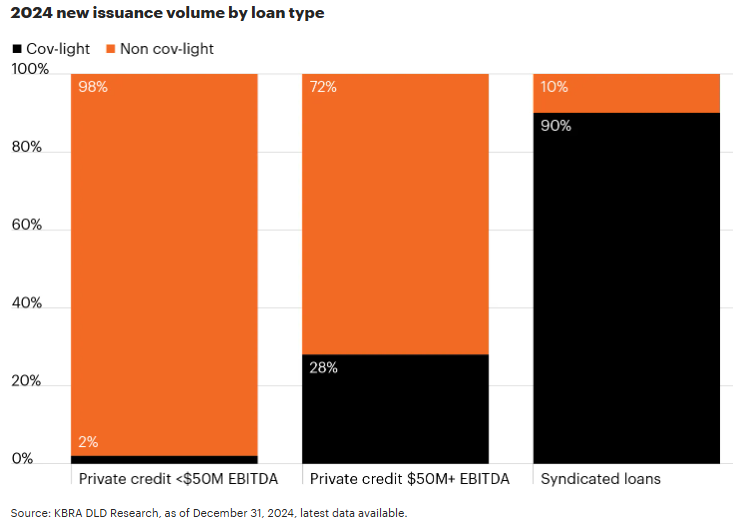

- Financial covenants exist across markets but vary significantly and generally receive much of investors’ focus. Syndicated loan documents have gotten progressively weaker over time, and now largely exclude financial maintenance covenants, and are thus considered “cov-lite”. Approximately 90% of new-issue syndicated loans issued in 2024 were cov-lite.1

The picture is very different in private markets, favoring investors with stronger covenants:

- In lower and core middle market direct lending, nearly all loans include financial maintenance covenants, with about half of all loans having at least two (usually a leverage covenant and an interest coverage covenant).

- In the upper middle market and large-cap space, where private credit increasingly competes with the syndicated loan market, only about 28% of deals are cov-lite.2

As discussed, today most new-issue syndicated loans drop maintenance covenants and rely on financial incurrence covenants instead. These only trigger financial tests when a borrower takes specific actions – like paying distributions or issuing new debt – rather than enforcing ongoing checks. Because they are reactive rather than proactive, incurrence covenants provide weaker lender protections than maintenance covenants.

What is the value of a covenant, and how does that change during stressed periods?

Loan covenants have real monetary value: they can restrict borrowers from taking actions that might harm lenders, and/or give lenders more power to minimize potential losses.

While it’s difficult to measure their exact value across the market, many studies have attempted to do so.

One study found that spreads on loans with a leverage ratio maintenance covenant were about 50bps tighter than those without, suggesting this covenant – which is common in private credit deals – may be worth roughly 0.50% annually to lenders.3

The value of covenants to lenders tends to lessen in calm, stable markets, but become much more pronounced during periods of market stress, when borrower financial weakness is more prevalent.

When economic growth slows and market spreads widen, more borrowers come under financial stress, often due to declining earnings and/or limited refinancing options. In these environments, strong covenants become far more valuable, helping lenders protect their investment by restricting harmful actions (through strict negative covenants) and enabling early intervention (maintenance covenants) if performance deteriorates. Financial maintenance covenants can give lenders early insight into such weakness – and the ability to take action to mitigate risks – in a way incurrence covenants do not.

How does FS incorporate covenants to protect investors?

Our $29 billion credit platform delivers tailored financing solutions across the middle market. Our strategies span senior credit, junior credit, credit secondaries and opportunistic private credit as well as a dedicated CLO business.

Each portfolio management team underwrites new investments to the terms and pricing that we believe are appropriate for the given market, strategy and opportunity. We leverage our size, scale and deep relationships to negotiate attractive risk-adjusted returns through both covenants and other risk management tools such as board observer rights, equity participation and personal/affiliate guarantees.

We generally avoid lending to private equity-owned companies where there’s an elevated risk of LMEs or potential lender disputes. We are also cautious of loans relying on aggressive EBITDA adjustments, favoring tried-and-true free cash flow as a more reliable measure of credit quality. When investing in the private upper middle market, where covenants are common but not ubiquitous, we take a careful deal-by-deal approach. For borrowers up to $100 million annual EBITDA, we generally insist on at least one financial maintenance covenant; for the largest borrowers, cov-lite structures check out only if we get adequately comfortable with the sponsor, the borrower’s financial health, and other terms of the transaction.

Beyond structural protections, we focus on overlooked markets that demand specialized sourcing, structuring and underwriting expertise. Asset-based finance (ABF) is a good example. We manage a business development company in partnership with KKR to invest in upper middle market companies and ABF, which are large pools of high quality hard and financial assets – like airplanes, recreational vehicles, receivables, mortgages or consumer loans – that generate a high level of cash flow. Because ABF performance is backed by contractual structures and/or tangible collateral, we believe it offers a strong complement to traditional corporate lending, which relies more heavily on future earnings and macroeconomic conditions.

Another good example is sponsored and non-sponsored lending to lower and core middle market companies. Our Global Credit Team manages a credit interval fund, a private business development company and a publicly-traded closed end fund focused primarily on lending to lower and core middle market companies. These are diversified businesses that are often overlooked by large credit managers due to their size, while their balance sheets may not meet the standardized criteria for traditional lenders like banks. As a result, we typically have a greater ability to negotiate favorable terms and structure investments that help mitigate downside risk.

In summary, we believe thoughtful downside protections can be a source of (under appreciated) investment alpha which becomes more pronounced in dislocated markets.

Sources:

1 Pitchbook.

2 KBRA DLD.

3 Abuzov, Rustam and Herpfer, Christoph and Steri, Roberto, Do Banks Compete on Non-Price Terms? The Dollar Value of Loan Covenants (May 2, 2023). Available at SSRN: https://ssrn.com/abstract=3278993 or http://dx.doi.org/10.2139/ssrn.3278993

Disclosure:

The views expressed in this Q&A blog do not necessarily reflect those of Heron, its affiliates, or representatives. Heron does not endorse or guarantee the accuracy or reliability of any statements made.

This content is for informational purposes only and should not be considered financial, investment, or legal advice. Readers should conduct their own research and consult a financial advisor before making any investment decisions. Heron is not liable for any losses or damages resulting from reliance on this information.