Private Credit vs. Private Equity: What’s the Difference?

Many investors are confused by the terms private equity and private credit (it doesn't help matters that the two are often classified as a single asset). This article breaks down the differences, including what types of investors are most suited for each asset class.

Get a diversified private markets portfolio built for market volatility.

The world of alternative investments is quite expansive, encompassing asset classes like real estate, cryptocurrency, precious metals and fine art. While those are fairly well understood by the general public, private credit and private equity can sometimes confuse investors who may have less exposure to these rather opaque sectors of the market.

Adding to the confusion is the fact that private credit and private equity are often grouped together as ‘cousin industries,’ despite their many differences. In fact, many large private equity funds manage private credit funds of their own.

It also doesn’t help that the two sound so similar–so if you’ve been conflating these two asset classes–we understand why!

In this article, we’re going to demystify private credit and private equity by exploring the features, benefits and drawbacks of each. We’ll also present the historical performance of each vs. the S&P 500, and explore which investor type is most suited to each asset class.

Key Highlights

- Private Credit is non-bank lending. It is subject to different regulatory requirements than bank lending, making it more flexible and available to businesses who can’t or won’t obtain a bank loan

- Private equity involves purchasing an ownership interest in a business. In contrast to private credit investors, who seek to earn a return on their investment through yield capture, private equity investors would like to see the business grow over time so they can exit at a multiple on their investment

- Private equity and private credit maintain unique benefits and drawbacks, making each strategy more appealing to investors based on their particular financial objectives and risk tolerance

What is Private Credit

The standard definition of ‘private credit’ is any non-bank loan where the debt is not issued or traded on public exchanges (one caveat here is that banks can issue private credit loans by launching specialized private credit funds, but these operate as separate investment vehicles).

So in other words, private credit takes place outside the conventional banking sector, which makes it subject to different regulatory scrutiny (more on this later). The loans are typically issued by non-bank entities such as private credit funds, private equity firms, hedge funds and specialty finance companies.

Private credit is gaining traction among small to medium-sized enterprises (SMEs) that may find bank loans inaccessible or seek more tailored financial solutions. As a result, the private credit market has expanded considerably, with institutional investors and high-net-worth individuals increasingly directing capital towards private credit, attracted by its compelling risk-return profile. This shift is evident in the growing number of private credit funds in the market (totaling 1,080 at the end of Q3 2023–a 19% increase from 2022’s total),[1] as well as the larger and larger deal sizes happening in the market, including Finastra Holdings’ $5.3 billion restructuring in 2023, which was the largest-ever private credit deal.[2]

Benefits and Drawbacks of Private Credit

Private credit offers several unique benefits for investors:

- Higher Returns than Stocks: From 1989-2023, the compound annual growth rate (CAGR) of the S&P 500 was 8.97%. Over that same time period, the median private credit manager’s CAGR was 11.32%.[3] That’s a hefty 2.35% difference per year!

- The Consistent Cash Flow of Bonds: Private credit investments offer regular cash repayments in the form of yield, which is captured by investors on the loans they issue to borrowers

- Lower Loss Rates than Many Other Asset Classes: The median private credit fund manager has never had a down year–another way of stating this is that said median private credit fund manager has produced positive returns every single year since the asset class first came to fruition[4]

- Predictable Returns: To be clear, private credit returns are unpredictable and based on numerous factors. That said, returns are more predictable than in other asset classes such as stocks or private equity, given that private credit typically produces regular cash flow to investors, and that the loans are scheduled to be repaid at a certain time. If all goes well, investors should expect a certain annual percentage yield (APY) throughout the duration of their investment, and a full repayment at the end of the investment lifecycle

Of course, the above is true if all goes well with a private credit investment. Sometimes, things go awry. With that in mind, explore the drawbacks inherent in this asset class:

- Illiquidity: Private credit is typically considered illiquid, meaning it can take many months or years for investors to recoup their invested capital (digital platforms are seeking to change this–more on that below)

- Credit Risk: Borrowers may perform below expectations, in which case they risk defaulting on their loans, which could trigger a partial or full loss of invested capital

- Interest Rate Risk: Investors in private credit may be forced to lock up their investment for extended periods of time. In these cases, there is the risk that the benchmark Fed Funds rate will rise. If the private credit investments are fixed rate, then a rising Fed Funds rate will eat away at the value of those recurring cash flows

In Conclusion: While private credit can offer attractive returns and the potential for consistent cash flow, there are also liquidity, credit and interest rate risks, which should be thoroughly examined by anyone considering investing in this asset class.

What is Private Equity

Private Equity (PE) is an investment strategy that involves injecting capital into private companies in exchange for an ownership stake in those companies. PE investors often play an active management role, seeking to enhance the value of a company before exiting through a sale or initial public offering (IPO).[5]

This form of investment is known for its high-risk, high-reward profile and requires a long-term commitment, making it suitable for sophisticated investors with substantial capital at their disposal.[6]

Benefits and Drawbacks of Private Equity

Much like private credit, PE offers unique benefits for investors:

- The Potential for Large Gains: PE is known for some major wins, with certain investors turning thousands of dollars into billions in some extreme cases (imagine owning a stake in Facebook back when it was called ‘The Facebook’)

- Active Ownership: Private equity firms often take an active role in managing their portfolio companies, as they seek to implement strategic and operational changes to improve performance. This can be advantageous to investors in these PE funds, who believe that the fund managers’ expertise will help drive revenue improvement and/or cost efficiencies[7]

- Potential Tax Advantages: Depending on the type of investment, PE can provide certain tax benefits. Writing off the interest on a loan secured to make an equity investment, investing in industries with tax incentives, and establishing a special purpose vehicle (SPV) for the purpose of investing in PE are just some of the ways that PE can potentially provide tax advantages[8]

And similar to private credit, private equity has some distinct drawbacks worth considering:

- Illiquidity: As PE investments are meant to grow the underlying business, they are often ‘locked up’ for many years, and typically investors cannot recoup their investment until an exit or IPO takes place (or investors sell their shares on a secondary market, if they can find a buyer)

- Lack of Transparency: As so much of private equity is…well…private. PE investors can lack clear visibility into what exactly the fund managers are doing, and whether their investments are being put to good use or not. While this drawback can also be applied to private credit, it tends to be far more pronounced with PE, as private credit funds are more ‘hands off’ vs. PE funds, which often take an active role in managerial and operational decision making

- PE is Hard: Perhaps the most dissuading aspect of investing in PE is just how difficult it is to pull off. PE managers must familiarize themselves with a business’ leadership, employees, culture, competition, industry, customers–all while increasing the valuation of the business to account for the premium they paid to acquire it (PE firms can purchase businesses at a discount, but those businesses typically have even more operational challenges than businesses acquired at a premium).[9] Remember, private credit funds don’t need to increase the business’ valuation, their primary concern is recouping their capital investment–so this drawback is unique to PE

In Conclusion: Private equity offers the possibility of eye-popping returns. That said, it requires skilled and effective fund managers to generate those returns, and investors typically need to wait many years before they can even begin to think about an exit.

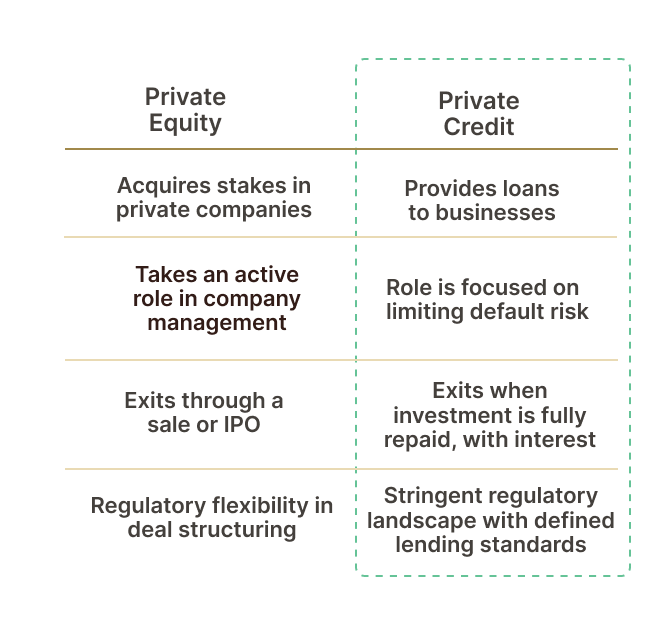

Differences Between Private Equity and Private Credit

At a high level, private equity entails acquiring shares in companies and (sometimes) participating in their strategic management. In contrast, private credit involves providing loans to businesses, focusing on generating returns through interest and fees rather than company ownership.

The below chart offers a handy guide to the particular distinctions of the two alternative assets:

Big Picture: Private credit is generally believed to provide more consistent returns than private equity, thanks to the interest rates that borrowers must pay. On the other hand, private equity carries a stronger risk / reward profile, due to its dependence on the growth and performance of the underlying company.

What Types of Investors Should Consider Private Credit and Private Equity?

While private credit and private equity are both alternative investments, they cater to different investor needs and preferences. Private credit funds typically attract investors looking for stable returns, while PE funds appeal to those willing to take on more risk for the chance of higher rewards. Both draw on capital from a mix of institutional and individual investors.

Of course, there is also the issue of liquidity to consider. Both asset classes are known for locking up investor capital for extended periods–something many individual investors might find off-putting–especially those who are used to investing in stocks and bonds, which can be liquidated at any time.

However, digital platforms are seeking to address these liquidity concerns.

Heron Finance is a digital platform that offers accredited investors access to private credit deals. The platform leverages blockchain technology to enhance its rebalancing capabilities, and is therefore targeting liquidity in as little as 30 days.[10] To be clear, this is not a guarantee of 30-day liquidity, rather an emphasis that the platform will make a best effort to meet redemptions in at least 30 days from request (read Heron Finance’s full approach to liquidity here.

As a lack of liquidity is one of the major sticking points for investors in both private credit and private equity, the ability to liquidate one’s private credit investment in only 30 days from the time of request could be a massive game-changer for those considering which alternative asset to invest in. Recognizing these distinctions can help investors make more informed decisions that align their portfolio with their financial objectives and risk tolerance.

If you are interested in learning more about private credit specifically, check out our article: “How to Invest in Private Credit.”

And to start investing in a diverse portfolio of private credit deals, click the button below.

Source: NYU Stern, data from Preqin ↩︎

Source: data from Preqin ↩︎

Source: Investopedia ↩︎

Source: Investopedia ↩︎

Source: Faster Capital ↩︎

Source: Faster Capital ↩︎

Source: Investopedia ↩︎

Source: Heron Finance reserves the right to modify the liquidity policy. Should there be any material changes to our policy, we will ensure all clients are promptly informed of these adjustments. ↩︎